Millennials are Reshaping the Real Estate Market – Here is how

Millennials are facing a major housing crisis in today’s market. The decisions they make now will impact their finances, lives, kids and reshape the overall market . What are most millennials choosing?

Millennials are facing a major housing crisis in today’s market. The decisions they make now will impact their finances, lives, kids and reshape the overall market . What are most millennials choosing?

If millennials opt to try and keep up with the perceived Joneses, they could find the additional financial burden a hefty one which limits freedom. But it isn’t an easy choice, as property prices soar, and friends and family scoop big homes.

The Globe and Mail highlighted how the Canadian housing market reflects the epitome of this dilemma. With the average price of a single-family home in some major Canadian cities pushing higher than $1 million, and even above $1.6 million, Canadian millennials have to choose between $1 million plus ‘starter homes’ or delaying household creation and having kids due to most of urban housing stock being one-bedroom rentals.

The CIBC chief economist says this is absolutely having an impact on household formation, and highlights difficult challenges ahead unless millennials can get over the stigma that comes with not having a single-family home with a yard. Unless reversed, this trend could clearly bring macroeconomic issues into play that impact the whole housing sector.

Some major American cities and regions are already mirroring what’s going on in Canada. Northern Virginia, New York, and Miami are just some of them. These cities are seeing robust building, with multi-million-dollar homes as the alternative. Inman News suggests over 60% of zip codes with top rated schools are now considered unaffordable. Even if it was legal, it’s hard to start a family in an urban micro-loft. Even those that can qualify for a $1 million starter home will be very tight on disposable income.

Rising home prices and talk of higher interest rates are putting incredible pressure on millennials to buy right now. It is highly unlikely interest rates will be this low again for at least a decade or two, if ever. The same goes for home prices. So, it is buy big now at great deals, or pay a lot more for the same home later. Home values could certainly dip temporarily as the cycle turns, yet, in the long run, values should just keep on going up. This is a chance to lock in low housing costs, equity, and even rental income.

However, there are cons to stretching finances and borrowing too much in this market – at least for millennials. It means little financial flexibility every month, in case of a downturn, or if life plans change. This is during the most critical and pivotal years for millennials, when income is still maturing, relocation is common, and the future is flexible. Let’s not forget this is a time for many major expenses.

So, what should millennials do? If you don’t buy real estate now, you’ll forever be financially dragging behind your peers, and your children will have less privileges than theirs. No one wants that. So how can millennials leverage current real estate opportunities without suffocating themselves with too much debt?

Buy a house, but buy one that is more affordable. Perhaps you can squeeze into a two-bedroom condo in the city, or buy a modest three-bedroom single-family home a little further out in the suburbs? Remember, these areas are likely to catch up to more central ones as cities expand on population growth. Others may find small multifamily properties are the smart buys. Buy and live in one unit, and rent the other out to reduce housing costs. Or, rent all the units out and use the excess cash flow to offset the cost of the house you really want. Invest for growth and income.

True Loyalty Properties is a full service real estate company that focuses on producing sound investments. We can help you buy, sell and invest real estate.

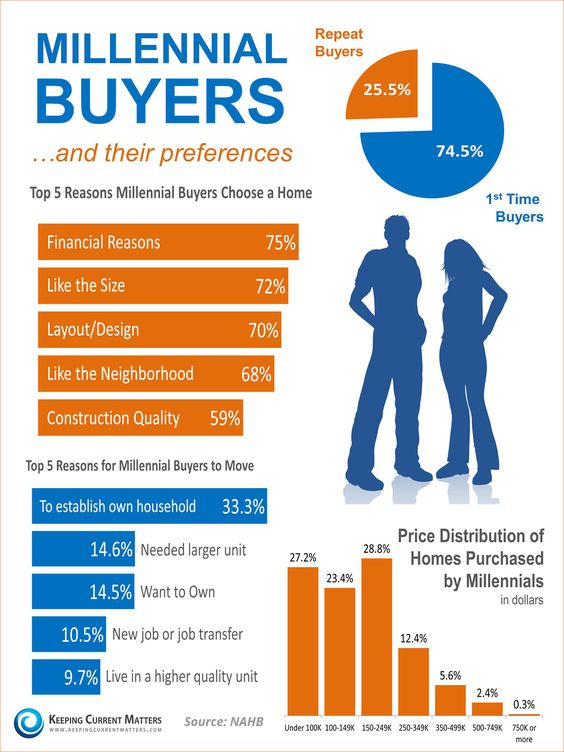

Millennial Stats